THE SMALL BUSINESS TAX DEDUCTION GUIDE.

Most of this blog post comes from the book Unf*ck Your Biz.

What’s a Deduction?

We call them deductions because they deduct from income. If you have $10 in income, and a $1 deduction, you deduct that $1 to have $9 in income.

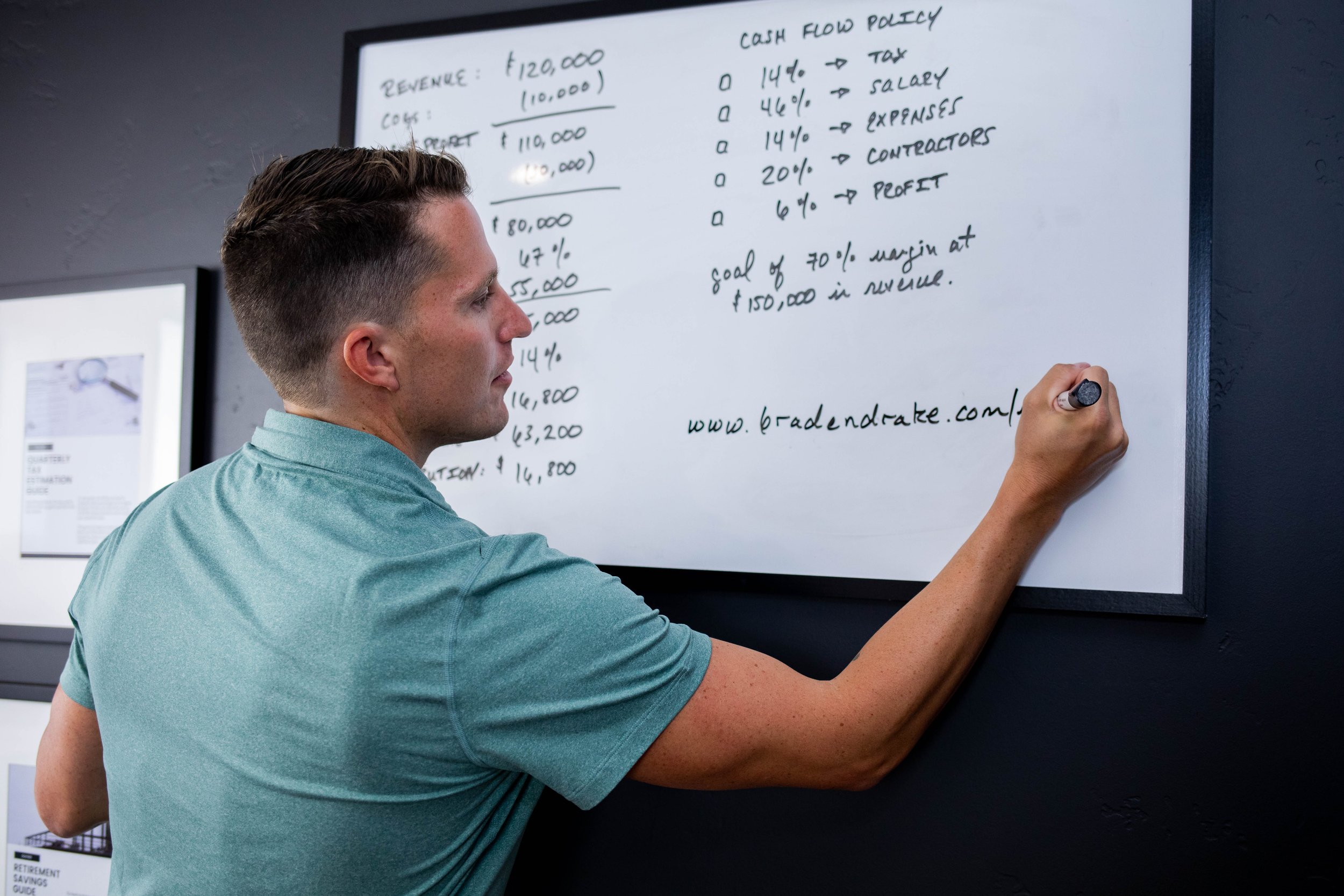

Business deductions reduce your gross business income to net business income. The IRS calculates taxes on the net business income. Assume for a moment that we have a flat tax percentage of 10%. The IRS, in this fictional universe, only collects 10% of all net business income.

If you have $100,000 in income, the 10% tax would total $10,000. Now assume you have a $10,000 deduction. How much are taxes now, and how much does that $10,000 deduction save you? Pause for a minute to do the math.

You deduct the $10,000 from the total income of $100,000. Thus, the net business income is $90,000. Now, the 10% tax is $9,000. In other words, that $10,000 deduction saves you $1,000 in taxes.

I highlight the net impact of deductions on your taxes because they’re often misunderstood by new business owners. Every November and December I talk to business owners who say something like “I need to invest some more in my business to lower my taxes this year.”

To me, this has never really made sense. Let’s break this down with some more realistic numbers. In Chapter 4, I explain tax brackets in more detail, but for now, note that we have graduated tax brackets, meaning the more you make, the more you pay in taxes.

So assume that you have $100,000 in net income with an effective tax rate of 21%. Your taxes would total $21,000. At the end of the year, you think, Well shit. I made a lot. That’s a lot in taxes. I should spend some more. You drop $40,000 in expenses: prepaying some stuff for the next year, buying courses, office furniture, and a new computer, and joining a pricey mastermind.

Now, net income is $60,000. If we assume an effective tax rate on $60,000 of 16%, your tax is now $9,600 (versus $21,000). The difference in tax is $11,400. You would have spent $40,000 to save $11,400.

Don’t think about deductions as free money. Think about them as a discount on whatever it is you’re buying. For example, assume that $10,000 of that $40,000 went toward a year-long mastermind. Look at that tax savings as a 30% discount. It’s like you saved $3,000 on that mastermind. Is the mastermind worth $7,000? Are you happy with that? If yes, awesome! Spend the money and take the deduction.

Use this type of analysis before buying shit to “reduce your tax bill.” If you need a new computer, buy a new computer and deduct it. If you don’t need a computer and spend $1,000 on one, but save $100 due to the tax deduction, you’re tossing away $900 that would be better off in your personal bank account. Deductions are great. Profit is better.

Make sense? Are you catchin’ what I’m throwing out there? Pickin’ up what I’m layin’ down? Bitchin’. Let’s now discuss what we actually can deduct. Let’s revisit the Schedule C. Give the form a Google and follow along.

First it asks for income and cost of goods. Technically speaking, costs of goods sold is not a deduction. (It has its own funky rules. We’re skipping over that.) When calculating net business income, you start by finding gross receipts (total business income). Then you subtract the cost of goods sold to find gross profit. For those of us who don't have costs of goods, our “gross profit” is the same as gross receipts.

From there, you add up all deductible expenses and subtract that total from the gross profit, in order to find the net business income.

What Can You Deduct?

Now our question is: What can we deduct according to the IRS? According to the IRS website, “To be deductible, a business expense must be both ordinary and necessary. An ordinary expense is one that is common and accepted in your trade or business. A necessary expense is one that is helpful and appropriate for your trade or business. An expense does not have to be indispensable to be considered necessary.”

SCHEDULE C

The Schedule C is the form you (or your tax software) fills out to report your business income if you are a sole proprietor or a single-member LLC. If some smarty-pants asks if you file a Schedule C, they’re effectively asking if you are a sole prop or a single-member LLC.

If you don’t have a business partner, and you haven’t formed a “formal entity” like an LLC or a corporation, you’ll be a Schedule C filer. Before continuing, take a second to Google “IRS Form Schedule C.” Open it and give a quick skim.

The lines in the expense section of the Schedule C show common categories and what’s allowed. Every IRS form also has a set of form instructions. These instructions tell you how to fill out various lines on the forms. Look at line 23 of the Schedule C, for example. You’ll find this is where you report deductions for taxes and licenses. But maybe you don’t know what the IRS considers to be a deductible. You can Google the IRS Schedule C Instructions and go to the section on line 23. It will tell you:

“You can deduct the following taxes and licenses on this line.

State and local sales taxes imposed on you as the seller of goods or services. If you collected this tax from the buyer, you also must include the amount collected in gross receipts or sales on line 1. . . .”

That part of the instructions lists several other taxes, but also goes on to state what you cannot deduct, including federal income taxes.

The tax deduction guide below essentially outlines the categories on the Schedule C form. Then, we will have additional, big-ticket-question deductions below that.

We’ve got more posts

If you want to learn more about how deductions work to reduce your tax and how to organize them in your bookkeeping, read this post.

Read about even more deductions

The Small Business Tax Deduction Guide

ADVERTISING

Advertising includes all marketing costs. One of the most common costs is one’s website. Other examples include Facebook ads, print material, including business cards, branded promotional items like mugs or stickers, and more traditional marketing items like print ads. Fees paid to sites like The Knot or Thumbtack would also go here. If you boost a post on Instagram, that’s an advertising expense. You get the picture.

Note that the materials are deductible as advertising costs, whereas expenses to create them (designer fees and ad manager fees) would go into the contract labor category.

CAR AND TRUCK

Under the tax law, you may take a deduction for business uses of your vehicle. You have a choice of taking either actual expenses or a standard mileage rate. If you use the standard mileage rate—this is the more common option—you simply multiply your business miles driven by the applicable rate. This is the more common option because it is simpler. One requirement to use the standard mileage rate is that you used the standard rate in the first year you used the vehicle in business. Thus, if you began with the expenses method, you will definitely want to track your expenses thereafter.

Standard Rate Method

If you choose the standard rate option, you need not track your car and truck expenses. However, you may take parking and toll fees in addition to the standard rate. Thus, if you are going to choose the standard rate, track all parking and toll costs, and then track your miles elsewhere (manual log or phone app).

Actual Expenses Method

This method allows you to deduct a portion of your actual expenses. You should track gasoline, car payments, car insurance, license plates, etc.

Important note: “Commuting miles” are not tax deductible. They are the miles driven between your home and your regular place of work. Only the miles driven from that location to your meetings and such are deductible. You can see now why the mileage deduction gets murky. Travel to meet a client from home or your office would be deductible.

How It’s Calculated: You don’t really need to know this. Your tax software is going to do the math. This explanation may just help you decide which method to choose.

Assume you traveled 3,000 miles for work this year. The 2020 standard mileage rate was $0.57.5. The deduction using the standard would be $3,000 x $0.575 = $1,725.

Now assume your total expenses were $100 per month for gas, a $300 per month car payment, and miscellaneous expenses totaled $1,000 for a grand total of $5,800. For the expenses method you need this total, and you also need to know the total number of miles driven on your car during the year. Let’s say your total miles driven is $12,000. Your 3,000 business miles amounts to 25% of the total miles driven, so 25% of your expenses are deductible: $1,450 (25% of $5,800).

In this example, the standard is better. The actual expenses method would get you a bigger deduction if your percentage of business miles compared to non-business were higher or if you had more expenses. Thus, the more expensive your car, the more likely the expenses method is the way to go.

Both methods require you to log your business miles. If you use the spreadsheet method for bookkeeping, you can track them manually or download an app like Mile IQ. If you use Quickbooks, the app has a great tool to help with this.

If you prefer the old-school approach, keep a notepad in your car. Each time you drive for work, include the purpose, as well as your odometer reading before you begin driving and once you arrive. I also like to include the difference between those readings, which represents the deductible miles, as well as a running total.

In addition to mileage, you can deduct: interest on a car loan, parking fees and tolls for business travel, and personal property tax on the car.

CLOTHING

I don't know why, but everyone wants to take clothing deductions for all the things. “I need more comfortable shoes because I stand a lot at work” is not a good enough reason to take a business deduction.

You may only deduct clothing if each of the following is true:

It is essential for your business;

It is not suitable for ordinary street wear; and

You don’t wear the clothing outside of business.

Theatrical costumes are a good example of deductible clothing. If you’re doing a local production of Wicked, you probably won’t be wearing your witch’s hat on a day-to-day basis.

COMMISSIONS AND FEES

This category includes fees paid for referrals, sales commissions paid to contractors, finder’s fees, and shared commissions in real estate, as well as transaction and processing fees.

The common ones are credit card processing fees (that money Stripe takes when you get a new payment) and referral fees paid out to influencers and affiliates.

CONTRACT LABOR

Contract labor includes payments made to persons you do not treat as employees, so basically the checks you send to independent contractors. Think second shooters, your virtual assistant, your social media manager, etc. Remember that you owe a 1099 to any contractors to whom you pay $600 or more.

In today’s modern biz world, you may be tempted to pay contractors via Venmo or PayPal, but I recommend checks or credit card payments. These are easy to track and remember come tax time.

Do not include payments made for “professional services or repairs” (discussed below). The professional services deduction is a bit misleading. That deduction is specifically for payments to accountants and attorneys for their services toward your business. Also, wages to employees have their own section. Other than those exceptions, include labor costs here.

COST OF GOODS AND INVENTORY

Cost of goods and inventory are often used interchangeably, but there is a bit of a difference. My friend Emylee from Boss Project has another business making and selling clay earrings. If she spends $100 on clay, she has $100 in inventory. This doesn't really become a cost of goods until she uses the clay for a product and sells it.

Let’s say she buys the clay in December. She estimates each earring contains about $5 of clay. She sells 10 pairs of earrings in December using this clay. Her cost of goods would be $50 and she’d have remaining inventory valued at $50.

Under the old tax rules, you had to “maintain inventory” using the following pain-in-the-ass formula:

Inventory at the beginning of the year

+ Purchases or additions during the year

– Goods withdrawn from sale for personal use

= Cost of goods available for sale

– Inventory at end of year

= Cost of goods sold

This bottom line is what then went on the P&L and tax return. As you can imagine, most small business owners messed this up. Luckily, we have new simplified rules. I encourage you to go with the new rule unless the old rules are working for you already.

Under the new tax laws, you may fully deduct all inventory if your business has annual gross receipts of less than $26 million per year for the last three years. I think that’s all of us.

This means we can give the middle finger to all of the complicated rules and simply deduct inventory when we purchase it like we would all other deductible expenses.

DEPRECIATION

The rules around depreciation are a huge pain in the ass, but they can be powerful for high-revenue businesses. Most of us, though, are not spending money on big-ticket assets, so I’ll keep this section relatively simple.

Assets that can be used in a business for more than one year must be depreciated. When you depreciate an item, you spread the cost out among multiple years. The rationale is that, for example, if you buy a computer, you use it for several years; therefore, you should deduct the cost of the computer over its “useful life.” Sounds unreasonable, right? While not to fear, there is a tax provision that allows you to fully expense assets in the first year of use rather than depreciate them. Put any depreciable property in this section.

Examples of depreciable property include office furniture, equipment like computers and tablets, software, and most other tangible items purchased exclusively for business. There is a gray area. An item like a stapler you would certainly use for more than one year, but we need not get too crazy.

IRS regulations provide a safe harbor to currently deduct an item in the year you purchased it if the item is $2,500 or less.

There are additional carve outs, most notably the 179 deduction. I won't bore you with the details, but this tax code allows you to fully expense long-term assets in year one up to certain amounts and phase-outs.

All you need to know/do is this: For any expense more than $2,500, you should keep a receipt and log it in your books as a depreciable asset. If you use a spreadsheet for bookkeeping, include the name of the item and the date purchased. When you or your accountant files the taxes, the software will guide the depreciation process.

EDUCATION

Education, like college courses, are deductible if you can show the education:

Maintains or improves skills required your existing business; or

Is required by law or regulation to maintain your professional status.

Undergraduate and graduate degrees typically aren’t deductible. Instead, this is more for things like required continuing education.

I used to include online programs like this one in education as well. After researching more for this updated book, I think I’d move those to contract labor or maybe create a “consulting” category.

GIFTS AND GIVEAWAYS

Deductions for gifts to clients and colleagues are limited to $25 per person. There is an exception for giveaways items if they cost $4 or less, have your name imprinted on them, and are an item you widely distribute. This would be something like a pen with your business name.

This is always where the categories could get wonky. I’d probably create a bookkeeping category for client gifts on their own. I’d lump giveaway items into advertising. Our categories for fully deductible expenses aren’t a huge deal since no matter where we put them, they are fully deductible.

WANT UPDATES ON TAX DEADLINES?

Join our monthly Newsletter where we send monthly legal updates, tax deadlines, and helpful guides and checklists.

HOME OFFICE

As you likely know, you may deduct expenses for use of a home office, but the rules are quite strict. You may only take the deduction if you:

Are in business;

Use your home office exclusively for business (unless you store inventory or run a daycare 🤷🏻♀️); and

Use your home office for business on a regular basis.

You must meet all three of those requirements plus one of the following:

Your office is your principal place of business (this is what would work if you only have a home office);

You regularly and exclusively use your home office for admin activities and have no other fixed location where you perform activities (this is what would apply is all the non-admin stuff takes places out-and-about);

You meet clients and customers at home;

You use a separate structure on your property exclusively for business purposes;

You store inventory or product samples in the space; or

You run a daycare center at home.

I’ll call this set of requirements the “additional requirements.” Note: You only need to check off one of the additional requirements. Most of us will easily meet one of the first two.

Let’s run through a common example. I used to have an office at WeWork, a popular co-working space. We also had a spare bedroom in our condo setup as a home office. Note I said it was set up as a home office. It wasn’t really my office. If I were working from home, it was usually on the sofa.

Was I in business? Yes. Did I use the home office exclusively for business? It'd be easy to claim that. There was only really a desk in there.

But, between you and me, we did put a blowup mattress in there for my niece and nephew when they visited. Let’s pretend we ignore that fact, and look at the “regular business” use requirement.

I didn’t use it that regularly, but let’s say I worked Fridays there and occasional weekends. That’d be regular. Now, we’d need to check off one additional requirement.

The office wasn’t my principal place of business. Option 1 is a no. Option 2 would also be out since I did admin work at my WeWork office. I could try to claim that I did all the admin work at home, but that’d be a stretch since I paid $900 a month for an office outside the home.

If, on the other hand, I paid the WeWork minimum of $250 a month for only common area space, I might be able to swing it. I could have done that for access to the conference rooms for client meetings only.

Mixed-Use Space

It’s pretty common to have a home office/guest room. On the surface, this is an issue with the second requirement—the “exclusive” bit. However, you can actually still take a deduction for the area of the space that is exclusively used for business. That could apply to half a room where you have your desk and maybe a guest bed. Or if you live in a studio or have a desk in a living room, you can section off your office area.

What You Can Deduct

The home office deduction is actually a bundle of deductions. You can deduct direct and indirect expenses. A direct expense would be something you buy just for your home office, like a desk chair. Note that’s technically a long-term asset subject to depreciation, but we would use the de minimus exception.

Most expenses will be indirect expenses.

Indirect expenses include rent, utilities, insurance, home maintenance (like house cleaning), HOA fees, and security system costs.

You can’t deduct your mortgage if you own a home but you can take a home depreciation deduction.

When prepping for tax season, simply brainstorm any and at all home expenses. Put them all on a spreadsheet or Google Doc and have them at the ready for your tax software or accountant.

How the Deduction Is Calculated

Like the car and truck expenses, there are two methods here. The first is the simplified method. This gives you a $5 deduction for every square foot of your home office up to a 300 square feet cap ($1,500). This method may be better for homeowners since you don’t have rent to include, but you gotta do the math.

If you’re paying rent, you’ll definitely want to use the pro rata method.

The pro-rata method allows you to take a pro-rata share of your expenses based on the square footage of your office in comparison to the square footage of your home. Come tax time, you will need to know rent paid, utilities paid, the square footage of your entire home, and the square footage of your home office.

For example, assume your home office is a 10x10 room, which is 100 square feet. Your home is 1,000 square feet, so your home office is 10% of the square footage. If your total, applicable home expenses total $15,000 for the year, your deduction would be 10% of that, or $1,500.

PROFESSIONAL FEES

This includes fees paid to accountants or attorneys for services related to your business. Why they have their own section outside of contract labor, I have no idea.

DEPRECIATION

Assets used in a business must be depreciated. When you depreciate an item, you spread the cost out over multiple years. The rationale is that, for example, if you buy a computer, you use it for several years; therefore, you should deduct the cost of the computer over its “useful life.” Sounds unreasonable, right? While not to fear, there is a tax provision that allows you to fully expense assets in the first year of use rather than depreciate them. Put any depreciable property in this section.

Examples of depreciable property include office furniture, equipment like computers and tablets, software, and most other tangible items purchased exclusively for business. There is a gray area. An item like a stapler you would certainly use for more than one year, but we need not get too crazy. There is a safe harbor rule for expensing rather than depreciating items with a cost of $200 or less.

Still a bit confused on this one? Start by asking yourself: “Will this item be used for more than one year?” If yes, and the item cost more than $200, it is a depreciable expense. If not, include it in another category. Don’t worry about how depreciation works precisely. Just know what items will go in the depreciation section of your tax return. Your preparer or tax software will walk you through the rest.

INSURANCE (NON-HEALTH)

Examples include general liability insurance and professional liability insurance. Health insurance is either an adjustment or a deduction on the tax return. That basically just means that it is not a business expense. Pay that out of your personal bank account.

LOCAL TRANSPORTATION

Business travel has all kinds of rules, but local transportation is fully deductible. Local travel includes any travel where you’re not away from home. “Away from home” means you have traveled somewhere where you won’t be staying at your house that night. If I attend a business conference in San Diego, my trips to and from would be local transportation and I could deduct Ubers, Lyfts, bus fares, and so forth.

MEALS

Business related meals are deductible if:

The expense is not lavish or extravagant under the circumstances;

The taxpayer, or an employee of the taxpayer, is present when the items are consumed; and

The food or beverages are provided to a business associate.

A “business associate” is any person you could reasonably expect to engage or deal with in business, so clients, referral partners, potential contractors, and the like.

The lavish or extravagant requirement is a subjective one. My husband took a trip with his best friend to the French Laundry, where dinner costs about $600 per person (alcohol not included), for his 40th birthday.

It’s a once-per-decade experience for foodies. If my business bestie and I decided to go, we’d inevitably chat business for a bit as always, but the IRS probably wouldn’t let it fly as a deduction.

The monthly $30 brunch I have with fellow San Diego entrepreneurs, sure! During Wedding MBA in Las Vegas, I may go out for a relatively nice dinner with business friends. I’m comfortable with that deduction. It’s reasonable based on the circumstances; I’m at a week-long, business event.

Sometimes meals are 100% deductible.

If you buy food for a holiday party, picnic, or for the general public for some type of marketing activity, that's 100% deductible. Also, if you're in a food business, like a restaurant, the cost of the food is fully deductible.

OFFICE EXPENSES

These are expenses for typical office supplies (e.g., pens, paper, computer ink, paper clips, postage, envelopes, etc.). Do not include your office rent or utility expenses. If you shop at Target or someplace similar, separate your personal and business transactions. Pay for the supplies with your business card. That will keep your receipts and bank statement nice and tidy.

TAXES

Deductible taxes include state and local sales taxes imposed on goods sold, real estate and personal property taxes on business property, federal unemployment tax, and federal highway tax. Deductible licenses are fees paid to state and local governments for necessary licenses. Federal tax payments are not deductible.

WAGES

Deduct here any salaries or wages paid to employees. Do not include amounts paid to yourself via distributions. Do include your wages if you, yourself are on payroll. Also, remember that expenses for contract labor have their own section.

TRAVEL

Deductible business travel is overnight travel away from your “tax home.” Your tax home is the city or general area of your principal place of business. If you live in a rural area, your general area is about a forty-miles radius from your principal place of business.

The trip must be for business. This may include attending seminars, conventions, or conferences, or traveling for business training/education, or to meet with potential clients and customers.

You can deduct transportation expenses and the expenses you incur at the destination. Your transportation includes flights, trains, buses, and rental cars, as well as 50% of meals and 100% of lodging incurred while traveling.

While at the destination, you can deduct 50% of meals, local transportation within the area, internet fees, and the like.

The meals bit is a bit confusing. When not traveling, we only deduct business meals—meals with other people, contracts, clients, etc. When traveling for business, every meal is a business meal, including the sad $12 sandwich I eat in the airport.

How Much Can You Deduct?

The amount of the deduction depends on where you’re traveling.

If you’re traveling within the U.S., you may deduct 100% of travel costs if more than 50% of the trip is for business use. So, for example, if you’re going to a business conference for four days, don’t stay and party for more than three. Also, your meals during the party days aren’t deductible. Sorry.

The rules for travel outside the U.S. are a bit more lax. If the trip is seven or fewer days, you can deduct 100% of travel costs, as long as you spend part of the time on business. You can only deduct the non-travel costs for the days you’re doing business.

For trips longer than seven days, you may take the full travel deduction if more than 75% of the time is spent on business. If less than 75% but more than 50% of the trip is for business, you may deduct a pro rata share of travel costs.

Meal Allowances

Rather than deducting the actual costs of meals while traveling, you also have the option to take a standard meal allowance. This is great if you forgot to use your business card or track meals while traveling, or if you aren’t spending much on your meals.

The rate you get per day varies based on the city and is set by the federal government. You can Google the per diem rates, but your software will do this for you. All you need to do is remember or note the dates and places you traveled.

SOFTWARE AND MONTHLY SUBSCRIPTIONS

I have read a lot of mixed guidance on where to put monthly business software subscriptions like Honeybook, Asana, Gusto, Quickbooks, and the like. I used to include them in office expenses. I no longer think that’s correct. Instead, I created a new category for them in my bookkeeping. I also like this because I get a very clear view of everything I have on auto-pay by viewing one line in my book.

SUPPLIES

Note that office supply expenses do not go here. Supplies are also not inventory or costs of goods. Supplies do not go into a final product that you produce, and depreciable assets are not supplies.

This always trips me up, so let’s break it down into examples:

Dressmaker

Sewing machine—depreciable asset

Fabric—cost of good/inventory

Needles—supply

Pens and paper—office expenses

Photographer

DSLR camera—depreciable asset

Client photo albums—cost of good

Camera bag and tripod (if less than $200)—supplies

If you’re wondering whether an item is a supply consider the following questions:

Is this an item that you will have for more than one year that cost $200 or more? If yes, it's a depreciable asset.

Is this an office expense?

If the answer to each of these questions is no, it's a supply.

RENT

This category is for your office rent if you have a dedicated office outside your home. It also includes rent paid for vehicle leases for business purposes.

UTILITIES

If you use a home office, you may deduct a portion of your home utilities bills such as water, electric, and sewage. If you are going to take these deductions, include your total utility expenses.

A NOTE ON MIXED-USE EXPENSES

Mixed-use expenses are those that are partially used for business and partially personal use. The most obvious and common example for all of us is our cell phones.

Between email and social media management, we spend a good deal of time working from our phone. We also use them to stay connected with friends and family.

Also, I use Facebook to kill time, but 50% of the time, I end up commenting on business posts, answering questions, etc. So how do we take a deduction for this?

The IRS allows us to deduct the business portion of the expense. Fifty percent is probably fine, but I deduct 70% of my cell phone bill. If I really did an accounting of my time, I bet close to 70% would be business use.

How to Account and Deduct

All the home office deductions are also mixed use. The best practice for mixed-use expenses is to pay them out of your personal bank account. Once you have an S corp (or partnership), you will actually have your business reimburse you with an accountable plan.

I WROTE A WHOLE-ASS BOOK, AND

I never thought people would be jazzed about reading a book on law in tax, but the reviews are in! And most read something like "I read this whole book, and I didn't hate it, and now I know stuff.

But for real, it walks you through my full "Unf*ck Your Biz Framework" - something I created for my first course, which was $2,000 and saw over 70 graduates - and is like the A to Z guide to get you started.

UNF*CK YOUR BIZ, THE BOOK -

UNF*CK YOUR BIZ, THE BOOK -

“I never thought I would say I enjoyed reading a book on taxes, but I definitely did. Braden’s wit and spunk made this, often times, traumatic topic of taxes, actually really fun and enjoyable. He put into perspective the proper ways of filing your taxes, as well as covering if you should become an LLC, S Corp or sole proprietor, for small business owners. It was jam packed with knowledge and key tips that I have already put into effect in my own business! I’m so thankful that Braden has decided to share his knowledge and help us small business owners. Highly, highly recommend reading this book and getting your legal stuff figured out!”

- Kelsey, Owner of Kelsey Rae Designs