SHOULD YOU HIRE A CONTRACTOR OR EMPLOYEE.

Most of this blog post comes from the book Unf*ck Your Biz.

Hi friend! Full disclosure. This is a complete redraft of this blog post. Here’s why. I’m a big believer in comprehensive education. My inclination is to teach you the history of this law, all the different exceptions, the temperature it was the day the law was drafted, you get the picture.

But here’s the thing. You don’t want to read all that shit. Thus, I’m giving you just the info you really need to get the answers you really want.

Before we get started, let’s get really clear on some vocabulary. “Employee” is a loaded legal term. When we call someone an employee it implies that they are entitled to a slew of legal benefits. When referring to someone who is not an employee, we typically use the term “contractor.’ I’ll use the term “worker” to refer to a person doing work for someone else when I’m not distinguishing between employees and contractors.

A DISCLAIMER

This post more answer the question “Can I legally hire a contractor, or do I have to hire an employee?” The non-legal-related pros and cons we won’t cover as much. I’ll touch on it a bit.

Also, note that these laws change all time. This post may not be 100% up-to-date. It’s not legal advice. And you should not solely rely on it to make legal decisions.

WHY WE CARE

When hiring or contracting with others, there are both tax and legal considerations. For the most part, the IRS doesn’t care as much about the legalities. They just want their taxes. Their interest is ensuring you’re not shorting them FICA taxes by misclassifying workers as contractors.

States do care about legalities. That’s because the states govern things like minimum wage and worker’s compensation. Therefore, the states make their own laws as to whether a worker is an employee or a contractor. You actually don’t get to make that decision, and neither does the individual you’re hiring.

You could both agree that the person you’re hiring will be working as an independent contractor. That doesn’t prevent the state in an audit, or the court in a lawsuit, from determining that individual should have been an employee, which would require you to pay them through payroll and cover certain benefits.

Misclassification of employees as contractors is a heavily litigated and high-risk area of the law, particularly in Left-leaning states that are cracking down on who can truly be a contractor. California even approved a $20 million budget allocation to enforce our new(ish) laws in this area. Enforcement seeks to uphold worker rights while also bringing in millions and millions to the state in payroll taxes.

Employees also have a lot of skin in the game. Being misclassified affects their taxes, disability, social security, and other employment benefits.

Many, many contractors are intentionally misclassified by employers. Courts are cracking down, and the rules are getting stricter. To stay in compliance and avoid lawsuits and penalties, it’s important to stay on top of the law.

Misclassification of employees as contractors is a heavily litigated and high-risk area of the law, particularly in Left-leaning states that are cracking down on who can truly be a contractor. California even approved a $20 million budget allocation to enforce our new(ish) laws in this area. Enforcement seeks to uphold worker rights while also bringing in millions and millions to the state in payroll taxes.

Employees also have a lot of skin in the game. Being misclassified affects their taxes, disability, social security, and other employment benefits.

Many, many contractors are intentionally misclassified by employers. Courts are cracking down, and the rules are getting stricter. To stay in compliance and avoid lawsuits and penalties, it’s important to stay on top of the law.

THE FRAMEWORK

I debated if I wanted to make this an A-Z guide type blog. I figure sure. You’re a smart cookie. You can handle it. Here’s where we’re headed.

(1) Learn the basic tests

Different states apply different laws/tests to determine whether someone can be a contractor or employee. Even more confusing, some states apply different tests to different areas of their employment law. 🤯 We will discuss the broad categories of tests first.

(2) A deep dive in emerging contractor laws

After we cover the basics, we will deep dive into California’s laws. Why? Well (1) we’re California based and (2) CA has the strictest enforcement, is the most populated state, and lots of folks are looking for answer. But also (3) Congress has considered passing federal law by adopting CA law, so it’s good to stay up-to-date with the trends.

(3) Figure out which state, AND which tests apply

Once you know how the tests work, we will discuss how to determine which states and which tests even matter for you.

THE TESTS

The key question here is whether a worker can be a contractor or if they must be an employee. Each state has their own rules, but almost all use one of two tests or variations of those tests. In this post, I’m aiming to give you the high-level overview of these tests.

Many creatives are in an odd position because the laws were seemingly written to crack down on large businesses that intentionally misclassify workers. Those laws are over-broad, sweeping thousands of small business owners into the new frameworks.

The rules are complex, new, and specific. The one in California implements a new test—one that is used in some form in about 30 different states—called the ABC test.

The ABC test is what we hip and cool lawyers call a “burden-shifting test.”

Under some laws, a worker was assumed to be a contractor. This means that if the worker wished to sue, claiming they were actually an employee, it’d be their responsibility to prove they were in fact an employee.

The ABC test flips the assumption.

If there’s a dispute as to the worker’s status, it’s the hiring entity’s responsibility to prove that person is a contractor. In other words, that worker is initially presumed to be an employee. It’s the responsibility of the hiring business to prove the worker either meets the ABC test requirements or one of many exceptions.

If you’re thinking, Ohh shit, that is the correct response. This is why we now must really have it together.

Under the ABC test, a worker must meet each of the following to be deemed an independent contractor:

A) The worker must be “free from the control and direction of the hirer,”

B) The worker must “perform work that is outside the usual course of the hiring entity’s business,” and

C) The worker must “customarily be engaged in an independently established trade, occupation, or business of the same nature as the work performed for the hiring entity.”

Parts A and C are relatively straightforward, so let’s start there.

Part A looks to the right of control and is similar to the analysis that would have taken place under the old law or under the common law tests. Circle back to this bit once you have read the “IRS or Common Law Test Section.”

Part C is most easily explained by example. If I, an attorney, contract with someone to take my brand photos, that contractor must be in business as a photographer. The same goes for one photographer who contracts with another photographer to second-shoot an event. The contractor must be “customarily engaged” in the photography business.

Here’s an example when Part C becomes a problem. Wednesday is a wedding planner. Their cousin April is in high school and wants a part-time job. April doesn’t have a business. April isn’t trying to have a business. If Wednesday hires April to be a day-of assistant, that would be a violation of Part C.

Part B is the stickiest issue. What it essentially means is that you can’t hire someone as a contractor if they do the same type of work as you. For example, a photographer couldn’t hire another photographer as a contractor, a graphic designer couldn’t hire another designer to assist them as a contractor—you get the picture. Those are the obvious examples. However, I like to ask following question as well:

Is the work the worker performs an integral part of the business?

And that could mean a lot of things. But think about what the “usual course of your business” is. I’ll use mine as an example. In our group programs, we offer Q&As, coworking calls, and bookkeeping office hours. Each of these assists our students and members work through our curriculums. An auditor would certainly argue that each of these things are within the usual course of my business.

In short, it seems that any task essential to the operations of the business in terms of clients/customer deliverables would be within the usual course of the business.

On the flip side, hiring a brand photographer to take new website photos, my editor to edit this book, and a graphic designer to make a new logo are all clear examples of things outside the usual course of my business. My business doesn’t do any of those things. We’re hiring outside help with area expertise for those limited-scope tasks.

The more gray area is where the tasks are not limited scope. They’re ongoing but not necessarily related to your client deliverables—for example, my social media manager or podcast editor. I pay these folks each and every month. Are those tasks within or outside the usual course of my business? I don’t think we have a clear answer yet, but I could put forth arguments on both sides.

So those are our As, Bs, and Cs, but that’s just the starting point. If you pass the ABC test, you’re not totally in the clear. You must then, in California, you must pass the Borello test (discussed in a bit). If you fail the ABC test, that’s not the end of the road either.

There are many carve outs and exceptions to the ABC test in California specifically, which I cover more below. If you are in California or plan to hire folks in California, make sure to keep reading. Although this is California-specific, it’s still helpful for everyone else since the state tends to be the trendsetter in this area of the law. Other states are beginning to follow suit. I won’t walk through all the exceptions and nuances here, but we can explore a couple relevant ones to our industries with a real-life example.

THE IRS OR COMMON LAW TEST

The IRS test is similar to the common law tests used across the various states that don’t use the ABC test. Instead of writing a 50-state treatise, I share the IRS test as the kind of counter to the ABC test.

The IRS uses a three-category “totality of the circumstances” test.

To explain how a totality test works, I like to compare it to RuPaul’s Drag Race. Stick with me. Ru says that America’s next drag superstar must demonstrate:

Charisma,

Uniqueness,

Nerve, and

Talent.

Sadly, it took me until season nine to realize this was an acronym. Anyhow, we’ve seen queens come and go with an overwhelming amount of charisma. They, I think, make the best TV. But maybe they haven’t fully developed in the talent category. However, Ru could determine their charisma so far outshines the others, and that, coupled with their uniqueness, nerve, and potential to grow their talent, warrants them being crowned.

Conversely, we may see queens with oodles of talent but little uniqueness, or tons of nerve without much else. The point is that these factors are a balancing act. Each judge may value certain factors differently. For me, it’s the charisma. Others may prioritize talent.

This is how a totality of the circumstances test works. It’s not a simple checklist. It’s a balancing act. Under the ABC test, you must check off A, B, and C. The IRS test is more fluid. She’s the non-binary diva in our drag pageant, so to speak.

The test looks at three overall categories. Here they are, along with descriptions, taken straight from the IRS website.

Behavioral: Does the company control or have the right to control what the worker does and how the worker does his or her job?

Financial: Are the business aspects of the worker’s job controlled by the payer? (These include things like how the worker is paid, whether expenses are reimbursed, who provides tools/supplies, etc.)

Type of Relationship: Are there written contracts or employee type benefits (i.e., pension plan, insurance, vacation pay, etc.)? Will the relationship continue and is the work performed a key aspect of the business?

Businesses must weigh all these factors when determining whether a worker is an employee or independent contractor. Some factors may indicate that the worker is an employee, while other factors indicate that the worker is an independent contractor. There is no magic or set number of factors that makes the worker an employee or an independent contractor, and no one factor stands alone in making this determination. Also, factors that are relevant in one situation may not be relevant in another.

The keys are to look at the entire relationship and consider the extent of the right to direct and control the worker. Finally, document each of the factors used in coming up with the determination.

WHY WE CARE ABOUT THE IRS TEST

Employers are responsible for withholding and paying a portion of their employees’ taxes.

The IRS uses this three-factor test to determine whether a business is acting as an employer. You may have a worker who is an employee at the state level but a contractor with the IRS. I have asked myself how this practically works. Answer: It doesn’t. This would simply mean if shit really hit the fan, you’d be SOL in state audits but okay in federal audits. It doesn’t mean you can continue working with contractors.

Thus, we need to know both the state and federal rules. Also, we need to detail these IRS rules, because some states have adopted the same test for state purposes.

STATE-BY-STATE CONTRACTOR CLASSIFICATION CHEAT SHEET.

Get access to this resource we created for our clients. We will email it to you when you join the backroom.

A DEEP DIVE INTO AB5 - CALIFORNIA’S CONTRACTOR LAW

Back in April of 2018, the Supreme Court of California made a decision in a case called Dynamex. The result was 80 pages of fun that completely reshaped the state’s employment laws. Specifically, it restructured the framework we use to determine whether a worker is an independent contractor or employee by implementing the ABC test.

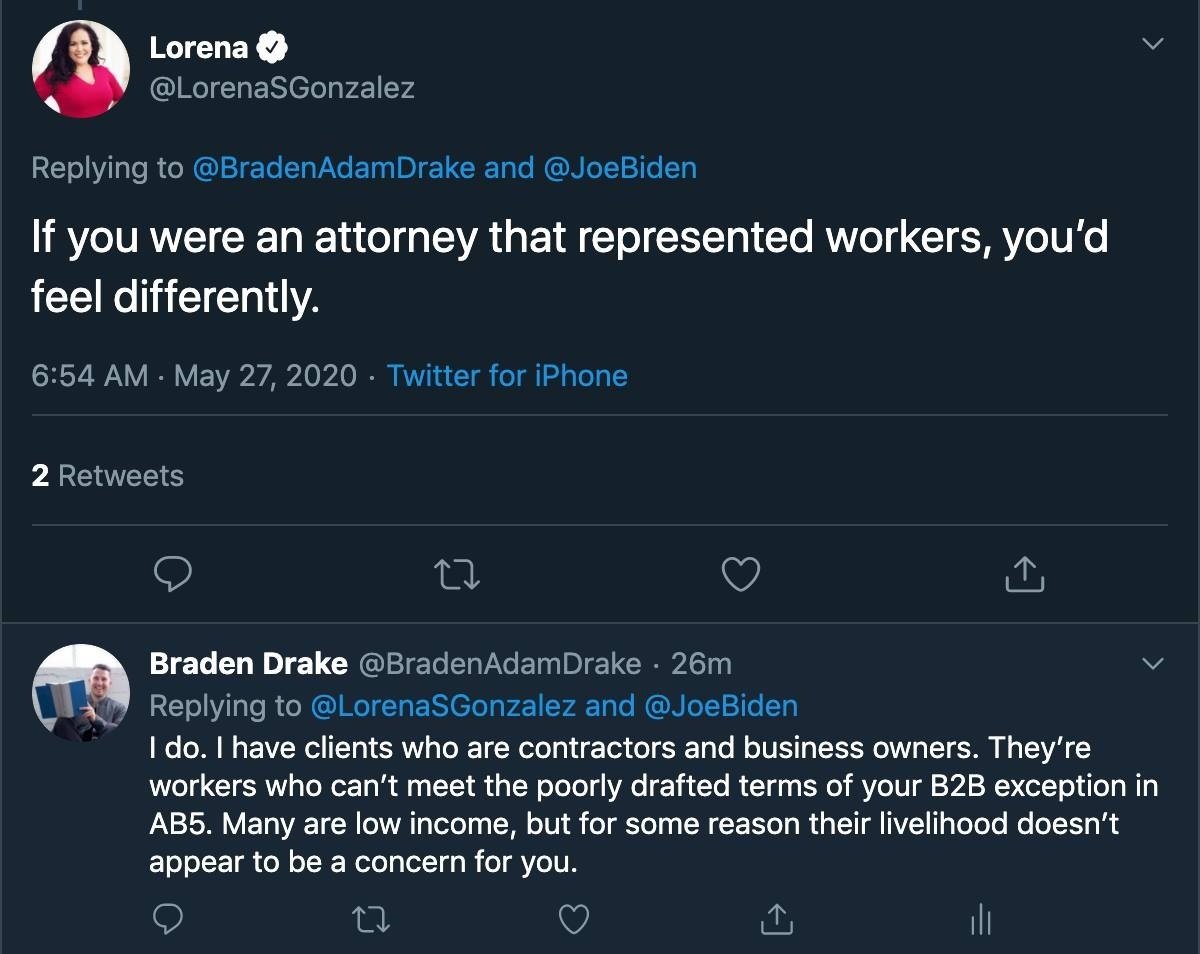

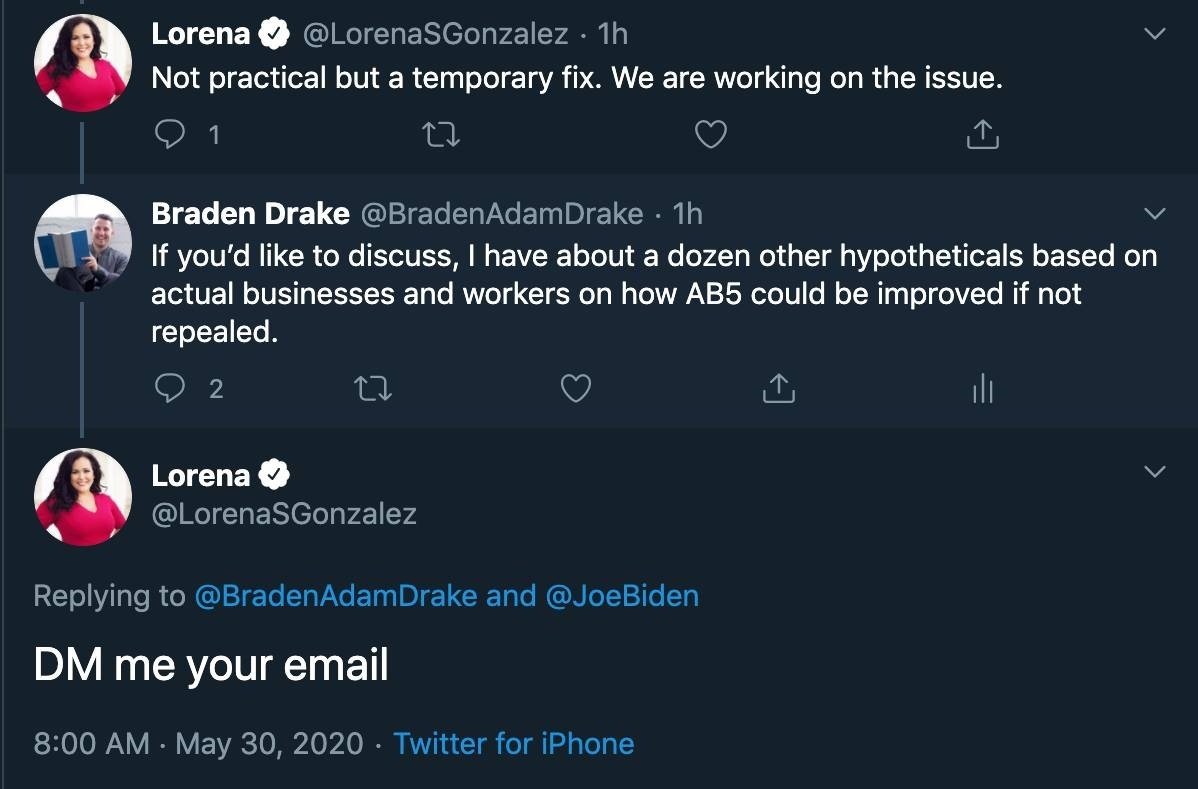

On September 18, 2019, the Governor signed into law Assembly Bill 5 (AB5). The law went into effect on January 1, 2020. AB5 codified the ABC test. Translation, it expanded the test to all areas of employment law and made the ABC test a big deal, officially. While the new law was largely a shit storm, it did provide many exceptions for various industries and professionals. But not really enough. It was still a hot mess. So much so, that I got into a bit of a twitter spat with the author of the bill. (I have the receipts. See the screenshots below. 😬😎😬).

Quick Update on This Twitter Saga

Assemblywoman Gonzalez actually did DM me her email. I drafted a 5 page letter with my thoughts on how AB5 could be best adapted for the event industry. Before emailing it, I got feedback from members of my Facebook Group.

I never did get an email response to the letter, but the the state did pass a “cleanup bill,” AB 2257. It was supposed to fix many of the previous issues. I’m sad to report that it’s failed in many respects.

AB 2257, the “Cleanup Bill”

The cleanup bill was largely passed to provide more exceptions to AB5 allowing more folks to be contractors. For the folks I work with, it specifically had the following provisions/exceptions…

The Single-Day Event Exception - which would theoretically provide exceptions to most wedding vendors

The Professional Services Exception

The Business-to-Business Exception

But before we dive into these, let’s cover two key points to keep in mind.

First, remember that we only care about all these rules IF a worker does not pass the ABC test. For example, if I hire a brand photographer, or a web designer, or an SEO strategist, or an HR consultant, they each:

Are dictating the scope and method of work, so they are free from the control and direction of the hirer,

They are providing work outside the usual course of my business, and

They have their own establish business doing the thing I’m hiring them to do.

They pass the ABC test. We don’t need to worry about all the exceptions and carve outs.

Second, if someone passes the ABC test, or one of the many exceptions do apply, that doesn’t automatically make them an employee. They must then pass the “Borello Test,” which is similar to the IRS test.

For a detailed breakdown of Borello and all the applicable AB5 rules, download our California, Contractor Compliance Framework.

Hang with me here bestie. I’m going to list some of the exceptions under AB 2257 here. Then, we will walk through with a real-life case study.

SINGLE-DAY EVENT EXCEPTION

The law defines a single-engagement event as a stand-alone non-recurring event in a single location, or a series of events in the same location for no more than once a week.

But, event pros, must meet 8 additional requirements to meet this exception.

(1) Neither individual is subject to control and direction by the other, in connection with the performance of the work, both under the contract for the performance of the work and in fact.

(2) Each individual has the ability to negotiate their rate of pay with the other individual.

(3) The written contract between both individuals specifies the total payment for services provided by both individuals at the single-engagement event, and the specific rate paid to each individual.

(4) Each individual maintains their own business location, which may include the individual’s personal residence.

(5) Each individual provides their own tools, vehicles, and equipment to perform the services under the contract.

(6) If the work is performed in a jurisdiction that requires an individual to have a business license or business tax registration, then each individual has the required business license or business tax registration.

(7) Each individual is customarily engaged in the same or similar type of work performed under the contract or each individual separately holds themselves out to other potential customers as available to perform the same type of work.

(8) Each individual can contract with other businesses to provide the same or similar services and maintain their own clientele without restrictions.

"Professional Services" Exception

There’s a whole group of service providers that fall into their own category of exceptions. AB5/AB2257 refers to these as professional services. I hate the name. It's confusing. But we gotta role with it.

First you must determine if you qualify as a provisional service provider. Some professions have a list of qualifications you must meet to be deemed a professional service. If you meet those qualifications, you must then meet 6 additional requirements as outlined below.

Photo & Video Professionals

Still photographers, photojournalists, videographers, and photo editors are exempt from the ABC test so long as:

The contractor works under a written contract that specifies the rate of pay and obligation to pay by a defined time, as long as the individual providing the services is not directly replacing an employee who performed the same work at the same volume for the hiring entity;

The individual does not primarily perform the work at the hiring entity’s business location, notwithstanding paragraph (1) of subdivision (a); and the individual is not restricted from working for more than one hiring entity.

(This does not apply to those who work on motion picture - don’t ask me why).

In addition, if you meet these requirements, you must also meet 6 requirements for professional services provides.

The 6 Requirements for Professional Service Providers

(1) The individual maintains a business location, which may include the individual’s residence, that is separate from the hiring entity. Nothing in this paragraph prohibits an individual from choosing to perform services at the location of the hiring entity.

(2) If work is performed more than six months after the effective date of this section and the work is performed in a jurisdiction that requires the individual to have a business license or business tax registration, the individual has the required business license or business tax registration in order to provide the services under the contract, in addition to any required professional licenses or permits for the individual to practice in their profession.

(3) The individual has the ability to set or negotiate their own rates for the services performed.

(4) Outside of project completion dates and reasonable business hours, the individual has the ability to set the individual’s own hours.

(5) The individual is customarily engaged in the same type of work performed under contract with another hiring entity or holds themselves out to other potential customers as available to perform the same type of work.

(6) The individual customarily and regularly exercises discretion and independent judgment in the performance of the services.

For a full breakdown & checklist of the requirements by industry, make sure to download the California Contractor Compliance Framework.

The Business-to-Business Catchall Exception

If no other exceptions apply, your final hope may be to meet the 12-point business-to-business exception. I’ve copied and pasted each exception directly from the law (that's the bolded portion) with a bit of my own commentary (in the unbolded portion).

(1) The business service provider is free from the control and direction of the contracting business entity in connection with the performance of the work, both under the contract for the performance of the work and in fact.

This really circles back to our original contractor laws. The has a checklist of factors for this that can help us analyze the issue of control. Check out the EDD Checklist.

(2) The business service provider is providing services directly to the contracting business rather than to customers of the contracting business. This subparagraph does not apply if the business service provider’s employees are solely performing the services under the contract under the name of the business service provider and the business service provider regularly contracts with other businesses.

Again, this isn’t really clear. What does providing services directly to the contracting business mean? Let’s look at an example. You hire a photographer to serve as a second shooter for a wedding. You have a contract. You tell the photographer the date and applicable details. The second shooter shows up, gets the shots needed and hands over the SD card to you. You then edit all the photos and send the gallery to the client. The second shooter never really communicates directly to your client.

Did the second shooter provide services to you or to your client? I would argue in this example that they're providing a service to you by operating as a second angle for photos and delivering the images to you. A state auditor, however, may disagree with us both since you are directly photographing the clients.

Where this becomes even less clear is when contracting with an associate photographer when you are not even present at the event. In that context, it looks more like the photographer is providing services directly to the client.

As you can see, this is more like a sliding scale. The more your contractor is in contact with your clients, the more likely they are to fail part two of this B2B exception.

(3) The contract with the business service provider is in writing and specifies the payment amount, including any applicable rate of pay, for services to be performed, as well as the due date of payment for such services.

This is the clearest requirement. You absolutely, 100% MUST have an independent contractor agreement in writing.

(4) If the work is performed in a jurisdiction that requires the business service provider to have a business license or business tax registration, the business service provider has the required business license or business tax registration.

Make sure your contractors have their required licenses. I have two suggestions for you here. First, require a copy of their business license before signing an independent contractor agreement. Second, add a warranty clause in your contract where the contractor warrants that they have all required licenses.

(5) The business service provider maintains a business location, which may include the business service provider’s residence, that is separate from the business or work location of the contracting business.

The contractor must, at a minimum have their own home office. Easy peasy. Luckily for us this was one of the provisions that got amended in the cleanup bill. It was super vague before.

(6) The business service provider is customarily engaged in an independently established business of the same nature as that involved in the work performed.

I find this requirement to a bit odd. The drafters are really just reiterating Part C of the ABC test. You may have also noticed that the first requirement in the B2B exception essentially incorporated Part A of the test. I feel like they almost could have said if you meet A & C of the ABC test but failed party B, then you can be exempted under a B2B contract if you meet the following additional 9 (rather than 11) factors, but I digress.

(7) The business service provider can contract with other businesses to provide the same or similar services and maintain a clientele without restrictions from the hiring entity.

This requirement is also pretty simple. You can't, in any way, restrict contractors from working with others. That includes your competition.

(8) The business service provider advertises and holds itself out to the public as available to provide the same or similar services.

This requirement is a little cloudy but clearer than others. Really just ask yourself whether your contractor is marketing themselves to provide the same service to others. If your hiring a VA consider whether they have a website or social media to promote those services to other potential clients.

(9) Consistent with the nature of the work, the business service provider provides its own tools, vehicles, and equipment to perform the services, not including any proprietary materials that may be necessary to perform the services under the contract.

You shouldn’t provide tools or equipment to your contractors. They need to be their own business and supply their own stuff. I have been asked several times something like “What if my second shooter needs to use one of my lenses during a wedding.” Ok, that may be fine, but you should have a whole set of gear on hand for your contractors.

(10) The business service provider can negotiate its own rates.

What does “negotiate their own rates” mean? Seems obvious, but I have found that this contradicts the way many creatives operate. Photographers and wedding planner often say, I pay X$ for day of help. That’s now a no-no.

My tip, allow your contractors to give the first offer for their rate. From there, you can absolutely negotiate, but try to ensure that your doing a relatively good job at compensating contractors according to their skill and experience. If you “negotiate” via email but end up paying all contractors the same amount, it ends up looking like a farce.

(11) Consistent with the nature of the work, the business service provider can set its own hours and location of work.

To me, the key here is “consistent with the nature of work.” If you’re hiring contractors for an event based contract, there is going to be a predetermined location and time. I’d assume and hope that’s A-ok. Contrast that with a web designer. Assume you run a marketing agency and outsource some web design work. It’s probably ok to say “We need this project completed by June 1st.” What you can’t do is require them to work at certain times or on certain days.

(12) The business service provider is not performing the type of work for which a license from the Contractors’ State License Board is required, pursuant to Chapter 9 (commencing with Section 7000) of Division 3 of the Business and Professions Code.

Most of us are not contractors in the construction sense of the term, so let's disregard this one.

A Real-Life AB5 Case Study

Jennifer Emmerling, photographer and owner of jenniferemmerling.com, was the first creative to come to me fighting an audit by the California Employment Development Department (EDD). This was more than three years after AB5 passed. In short, Jennifer got pulled for a “random audit,” according to the EDD. Jennifer sent 1099s to two different second photographers in 2020. Both photographers worked single-day events alongside Jennifer as contractors. The EDD audited Jennifer in 2023, arguing the photographers should have been employees.

Because Jennifer is a photographer and she hired photographers, she clearly failed part B of the ABC test. We argued each of the three exceptions above applied, making the photographers contractors, not employees. Let’s look at how this actually shook out.

SINGLE-DAY EVENT EXCEPTION

In Jennifer’s case, the EDD said she failed the requirements because…

“[w]orkers are not free from the control and direction of the hiring entity. During the shoot, Jennifer gave directions to workers: whom to follow, what segment to cover, which lens to use and which angle to take for a certain scenario per Jennifer’s preference. Workers were given instructions about the way the service was to be performed. Jennifer explains the timeline of the event to workers and they worked together to coordinate the photography needs.”

This speaks to the “control and direction” requirement. You see this requirement in almost every test and exception. We made counterarguments to this explaining how we believed Jennifer collaborated with the other photographers so they could get the correct number of shots at various angles, etc., but they didn’t seem willing to budge.

The EDD did not take issue with the other seven requirements under this exception.

BUSINESS-TO-BUSINESS EXCEPTION

Under this exception, the EDD made the same “control and direction” argument and stated the “workers provided services to the clients of the hiring entity,” rather than to the hiring entity itself (Jennifer) as required under the exception.

Essentially, they were saying that since the photographer was taking photos of and for the client, they couldn’t utilize the B2B exception. We argued the second photographer worked for Jennifer since Jennifer hired the photographer and that photographer delivered the photos to Jennifer. The EDD didn’t agree.

This is, in my opinion, one of the dumber requirements of the whole law.

PROFESSIONAL SERVICES EXCEPTION

Under this exception, the EDD originally claimed two requirements were not met, stating:

“Workers are not able to set their own hours. The shooting schedule is set by the hiring entity and their client.”

and

“During the shoot, Jennifer gave direction to workers. . . . It does not appear that workers could exercise discretion in the performance of the services.”

We countered both of these arguments with our own, and the EDD ended up accepting those arguments allowing the second shooters to be contractors. Yay!

To the first point, requirement two of six of the professional services exception states: “Outside of project completion dates and reasonable business hours, the individual has the ability to set the individual’s own hours.” We argued that the project completion date was the wedding date. Therefore, it’s reasonable that it could not be changed. However, outside of that date, they could set their own hours to fulfill any other aspects of the contract. Check.

Here’s requirement six: “The individual customarily and regularly exercises discretion and independent judgment in the performance of the services.” Notice how this is similar to, but less strict than, a “control and direction” test. It simply requires that the worker regularly exercise discretion. That doesn't mean the hiring entity can’t exercise some control. We made the same arguments that we had asserted for “control and direction,” which were successful here.

Maybe you now see why lawyers are notoriously difficult. We’re trained to argue over the finest details that can make or break a case.

The Big Takeaways for Creatives

As you can see from the case study, the state interprets “control and direction” extremely strictly, and most exceptions have a control and direction element. The Professional Service Exception doesn’t, but that currently only covers:

Freelance Writers (with some additional requirements)

Graphic Design

Content Contributors

HR Administrators

Payment Processing Agents

Photo and video pros

Marketing professionals

Fine artists, and

Beauty professionals

This is not a comprehensive list. Each highlighted bullet has additional requirements.

Things You Must Do

Due to the various exceptions and requirements, I now recommend all business owners to:

Have a signed contract with every contractor for every project/event,

Get a copy of each contractor’s business license,

Verify that the contractor is marketing their own business in some way.

Some Notes for Wedding/Event Pros

I don’t want to give a full breakdown of how the exceptions apply to every type of vendor, but let’s think broadly here. What makes this extra tricky is differentiating between who I, other wedding pros, and reasonable people think should pass the tests, versus what I’m assuming the state would argue.

The EDD is seemingly arguing that any control and direction is too much. Consider that each person you might hire could fall into one of three categories.

The contractor is the expert and they decide what needs to be done. E.g. A rental company hires a delivery company to deliver rentals.

Both the contractor and the hiring entity are equal experts. Eg.g. photographer hires second shooter or floral assist hires another floral design to assist on a project.

The hiring entity is the expert and the contractor is a non-expert, non-business owner. E.g. wedding planner hires friend or family member to help as a day-of-assistant.

I used to be of the opinion that, in most circumstances, folks in 1 and 2 would meet one or more of the exceptions and that folks in part 3 would not. Now, I see that the state is likely only going to allow the zone 1 people pass. We won’t really have much more to work with until businesses start to appeal the decisions and work their cases up the courts.

Some Notes for Online Business Owners

Course creators, membership owners, educators, speakers, consultant, and generally online business owners live in their own segment of the modern day business world. Many of us are all virtual. We hire virtual assistants, social media managers, and community directors. We can look to the B2B exception, but I think we first need to step back and really focus on Part B of the ABC test.

B) The worker must “perform work that is outside the usual course of the hiring entity’s business

If a worker is outside the usual course (and meets A and C), we are out of the woods with regard to AB5. So who is within the usual course and who is not. I think we can break this into three kind of categories as well.

Someone is obviously within the usual course. E.g. You run an ad agency and hire folks to help run your clients ads.

Someone is providing services integral to your business. E.g. You hire someone to handle billing issues, or manage your online communities.

Someone is providing services to your business unrelated to your business. E.g. You run an ad agency and hire a photographer to take your website brand photos.

Can you see how category one clearly fails part B and category three clearly passes? Number 2 is the dicy area. And this examples could shift. For example, what if the ad agency hires a photographer to take photos they will use in a client’s ads? I’d put that in category 2. Is that within the usual course of the hiring entity’s business? I could and would argue no, but I’d bet the state would argue yes.

All the templates you need. All in one place. Just pay the cover, and you’re in for life.

We’ve got more posts

Knowing these rules is huge, but they all fall into the broader context of your legal essentials and strategy. And we have more on that for you…

THE DIFFERENT AREAS OF LAWS

Employment law is a bundle of laws. The general areas of concern are:

Unemployment insurance

Worker's compensation insurance

Wage & hour laws

Civil rights stuff

When determining whether a worker is or should be a contractor or employee, different tests may apply in these different areas. Meaning, a state could use the ABC test to determine whether a worker should be an employee for purposes of unemployment insurance but the IRS test for the purposes of wage and hours laws.

Let's quickly breakdown these four categories.

Unemployment insurance is a fund controlled by the state. If have an employer and lose your job, you can file for unemployment and receive monthly payments from the state. This money comes from a fund, which is funded by the employers that pay into it. Employers must pay into the fund when they have employees. Thus, the worker classification issues determines whether you'd need to pay into the fund when hiring a worker.

Businesses get in trouble with unemployment insurance when their worker's file for unemployment. This was a recurring issue during the COVID shutdown. Workers were filing for unemployment. When doing so, they must note who their employer was. Can you see the issue? They were stating a business was their employer when the business thought they had a contractor.

This gets tricky because worker classification is not a choice. It's a determination, mostly. It's law. Like the speed limit. If the speed limit is 70, you can drive 80 basically every day, like I do, and maybe be fine, but you know that's above the limit. You can't just decide the speed limit is whatever you want it to be. Going over is a gamble. However, you can always drive under.

Hiring is similar. The limit, or threshold issue, is whether someone should be a contractor or employee. You can't decide someone will be a contractor if the laws state they must be an employee, nor can the worker. However, someone that can legally be a contractor, could be hired as an employee instead.

If a worker files for unemployment, the state may not care if you had them sign an independent contractor agreement. They only care about whether that worker would meet their test for determining whether a worker can be a contractor. If the answer is no, you may be in trouble.

These same concepts apply in the other areas as well.

Businesses obtain worker's compensation insurance to pay out potential, work related injury claims. Some states have their own factors on whether a worker is an independent contractor for worker's comp purposes. I wasn't so sure how this worked in practice, so I actually called the state of Wisconsin, which uses separate tests for basically everything.

Unemployment insurance (UI) is generally setup through payroll. Once you onboard someone as an employee, the payroll provider will walk you through the UI steps. Worker's comp is obtained through private insurance companies.

It's possible, in a state with different tests, to have a worker who doesn't need to be an employee for UI purposes but who does need to be covered by worker's comp, in which case, you could get them covered without technically making them an employee. You'd be covered in that case. Confusing, I know.

The next area of concern is wage & hour laws. Again, this is a bundle of laws. These are primarily related to how much employees must be paid per hour, and whether they need to earn overtime, among other issues.

Very broadly speaking, if you're paying your worker's well above minimum wage and not dictating their hours worked, you likely need not stress to much about these laws.

Lastly, we have our civil rights laws. These govern discrimination issues, hiring and firing practices, and more. I find that we generally have an intuitive understanding of what is allowed, but I recommend working with a well-qualified HR consultant or employment attorney to be aware of what you can and can't do when it comes to hiring, firing, and generally working with employees.

PRACTICALLY SPEAKING…

If someone would need to be an employee under any area of law, it’s probably best to just hire them as an employee. It’s not quite that simple, but it’s also not quite worth it to get more complicated than that. But in our State-by-State Contractor Classification Cheat Sheet, we give a break down of the tests used for each area of law in each state. But more importantly, we try to break it down into practical basics.

YOUR STATE LAWS

We covered the basics to give you a rough idea of the various contractor classification tests and how they work. Now, it’s time to do some research. Your goal is to find what test is applicable in your home state, along with the test in each state in which you have contractors or employees. Apply the controlling test in the state in which the worker you’re hiring is based.

BUT, before you spend all your free time, doing all the research, you may just want to check out our quick guide. It’s a State-By-State Contractor Classification Cheat Sheet.

About 33 states use some version of the ABC test. Some of those are modified and some apply the ABC test to only portions of their employment laws. This is why state-by-state research is key.

Try searching “[state name] test for independent contractor.” I did this for several states. If you want to search along, do a search for Tenessee. It is an interesting one.

I did the search. One source said they used the common law test and one source claimed they used the ABC test. Look for resources with a .gov address. They should have the most up-to-date information. When I searched, I found a tn.gov link. The state website clearly shows a change in law effective January 2020.

It said, “For services performed BEFORE January 1, 2020, the law in effect is the ‘ABC’ test.” Lower down, it stated, “For services performed ON or AFTER January 1, 2020, the law is the 20 factors,” which is similar to the IRS test.

I point this out because it also demonstrates the regular updates in law and the importance to stay on top of the changes. While researching, I noticed an interesting trend: Many Left-leaning states have been adopting the ABC test. That didn’t surprise me. The interesting part was that there were more states—conservative states—that have begun to move away from the ABC test.

I expect most states to continue making updates for several years. We should also watch for federal changes in this area of the law.

STATE-BY-STATE CONTRACTOR CLASSIFICATION CHEAT SHEET.

Get access to this resource we created for our clients. We will email it to you when you join the backroom.

THE HIRING PROCESS

To talk about the hiring process or not to talk about the hiring process? That was a big question for me. Ultimately, I decided to take one of my favorite approaches: I’m giving you the basics and encouraging you to seek additional help, particularly if you need to hire an employee.

This whole chapter has been dedicated to determining whether you can hire a contractor or if you must hire an employee.

You can think about hiring employees as a three-step process:

Find the right candidate

Onboard the person

Stay compliant

A lot of folks only consider number two, but hiring the wrong person or for the wrong role creates its own problems. Once you do find that person, you should ideally have a company handbook and do proper onboarding. Then, you need to comply with all the local, state, and federal laws. It’s a lot, which is why I rely on HR experts to help my clients and me. If you need to or want to begin to hire employees, consider this a necessary investment in the health of your business.

I WROTE A WHOLE-ASS BOOK, AND

I never thought people would be jazzed about reading a book on law in tax, but the reviews are in! And most read something like "I read this whole book, and I didn't hate it, and now I know stuff.

But for real, it walks you through my full "Unf*ck Your Biz Framework" - something I created for my first course, which was $2,000 and saw over 70 graduates - and is like the A to Z guide to get you started.

UNF*CK YOUR BIZ, THE BOOK -

UNF*CK YOUR BIZ, THE BOOK -

“I never thought I would say I enjoyed reading a book on taxes, but I definitely did. Braden’s wit and spunk made this, often times, traumatic topic of taxes, actually really fun and enjoyable. He put into perspective the proper ways of filing your taxes, as well as covering if you should become an LLC, S Corp or sole proprietor, for small business owners. It was jam packed with knowledge and key tips that I have already put into effect in my own business! I’m so thankful that Braden has decided to share his knowledge and help us small business owners. Highly, highly recommend reading this book and getting your legal stuff figured out!”

- Kelsey, Owner of Kelsey Rae Designs